United Kingdom

United Kingdom Argentina

Argentina  Australia

Australia  Austria

Austria  Brazil

Brazil  Canada

Canada  Germany

Germany  Ireland

Ireland  Italy

Italy  Malaysia

Malaysia  Mexico

Mexico  New Zealand

New Zealand  Poland

Poland  South Africa

South Africa  United States

United States European stocks rebound as ECB rate cut bets increase

Share:

Europe

The last few days have seen European markets seek to reverse the damage of the early part of last week, but it has been slow progress higher, with the FTSE100 underperforming relative to its peers.

We opened the session with a modest pullback on the gains of yesterday as markets took stock against a backdrop of disappointing economic numbers, and a reluctance on the part of central banks to consider the prospect of early rate cuts.

Today’s ECB press conference may have seen a slight dovish shift in the prevailing narrative here of no early rate cut, although the ECB might seek to deny it.

The catalyst for this possible shift could have been yesterday’s awful PMI numbers, or this morning’s German IFO survey which saw a further deterioration in economic activity in January and pointed to a further decline in optimism about the prospects for the German economy. Companies were more pessimistic about the outlook than they were at the end of last year with the reluctance of the ECB to consider an early rate cut most likely to have soured business optimism.

This afternoon’s decision by the ECB didn’t contain any surprises with rates left on hold, with the accompanying press conference a broad word salad of jibber-jabber in parts as ECB President Lagarde tried to convince the markets that a rate cut before June was not a realistic possibility.

All of that aside, if you managed to pay attention for long enough there was one noteworthy comment which markets do appear to have reacted to. Her insistence that talk of rate cuts was premature, echoed comments made earlier this month. Despite this the possibility of a cut wasn’t completely ruled out, which keeps the prospect of an earlier move on the table and has helped to drag European markets off their lows of the day, and back into the green.

US markets also opened higher after US Q4 GDP slowed from 4.9% to 3.3%, well above forecasts, although a larger than expected slowdown in the GDP price index to 1.5% from 3.3% kept the current goldilocks possibility of a March rate cut alive and kicking.

Some notable gainers on the back of the US Q4 GDP print were equipment rental provider Ashtead Group which rents industrial and construction equipment in the US, and where it gets 80% of its sales, with the shares popping higher on the back of the stronger numbers out of the US.

The energy sector is also getting a lift on the back of firmer oil prices after US inventories came in below expectations, with BP and Shell edging higher.

Wealth manager St. James Place is one of the worst performers on the FTSE100 after reporting that inflows slowed to £5.1bn last year, as higher savings rate tamped down on demand for its services.

With easyJet reporting a solid set of numbers yesterday, Wizz Air shares have slipped back after Q3 losses came in higher than expected at -€105.4m, despite an increase in revenue of 16.8% to €1.06bn. The grounding of some of its fleet for mandatory engine inspections, along with the cancellation of its Israel routes hasn’t helped.

There’s not been much of a reaction to the news that Haleon is selling its ChapStick brand to Suave Brands for $430m.

US

US markets opened higher after US Q4 GDP came in well above expectations, and the core PCE price index slowed to 2%, while weekly jobless claims rose from 187k to 214k.

US tech stocks continued to look resilient despite a disappointing set of Q4 numbers and outlook from Tesla as the first of the so-called Magnificent 7 to report.

The last few months have seen Tesla shares trade sideways as doubts about its ability to grow sales and maintain margins has increased. These doubts appear to have been confirmed after Q4 revenues rose 3% to $25.17bn but fell short of forecasts of $25.9bn.

Profits were also below expectations coming in at 71c a share, while automotive gross margin fell from 28.5% to 18.2%, with Tesla declining to offer an outlook for 2024, which in a sense was quite revealing. In the past Musk has rarely shied away from being bullish on the outlook, however yesterday he was quite downbeat opting to reflect on the challenges facing the business, especially from BYD in China as well as more globally. Tesla’s miss has also translated into weakness across the sector with Lucid and Rivian also on the back foot.

Boeing shares are also under pressure after the Federal Aviation Authority called a halt to the production of its 737 MAX production line until it is satisfied that its quality control procedures are robust and have been resolved. The move while necessary only adds to the problems for Boeing at a time when its reputation for quality has taken a huge knock. The revelation that checks on other Boeing jets have shown up problems has sown further doubt about the company culture and its attitudes to customer safety.

On the plus side IBM shares are higher after the company reported Q4 results that were better than expected, while also upgrading its outlook for 2024. Revenue for Q4 came in at $17.38bn, while margins improved to 60.1%, and profits came in at $3.87c a share. Free cash flow was also strong surging by 17% year on year to $6bn. For 2024 the company estimates FCF of $12bn and mid-single digit sales growth pushing the shares to 10-year highs.

Microsoft shares have edged higher after the company announced that it was cutting 1,900 Activision and Xbox staff as it looks to cut costs as it integrates the business after completing the recent takeover.

FX

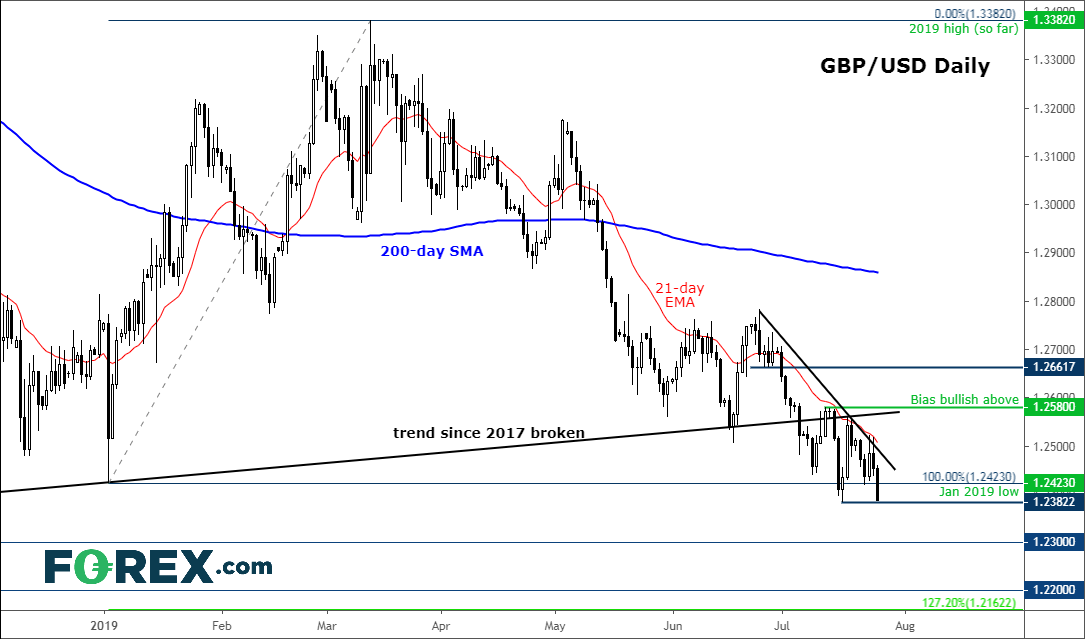

On currencies the pound pushed up to a one-week high yesterday on the back of a strong services PMI number in January, however that resilience has taken a knock today after a truly dreadful set of retail sales figures from the CBI which saw sales volumes hit their lowest levels in 3-years.

The euro slipped back to the lows of the day after ECB President Christine Lagarde pushed back on speculation about a rate cut before the summer, insisting that such talk was premature, echoing comments made earlier this month. It was noteworthy that the possibility of a cut wasn’t completely ruled out, and it is that markets are reacting to, which does keep the prospect of an earlier move on the table. This has seen German 2-year yields push sharply lower, with the next ECB meeting set for 7th March. Perhaps an April rate cut isn’t as fanciful an idea as it was a few weeks ago?

Commodities

Crude oil prices have pushed up to their highest levels in 8-weeks after a fall in US inventory data showed that demand is more resilient than feared, although the sharp cold snap may well have played a big part in that decline. US oil production remains at record highs which may have the potential to cap gains in the short term, however the better-than-expected US economic data also shows that the US economy is more resilient than thought.

Gold prices still appear to be treading water but have edged higher on the back of softening yields in Europe and increasing expectations of an ECB rate cut by the summer.

Volatility

Wednesday proved to be something of a mixed session for several greenback trades, with the AUD/USD pair proving to be one of the most active. Improved Aussie PMI on Tuesday had offered some momentum, but better than expected comparative prints from the US served to draw a line under gains, kicking off a complete reversion. One day vol on AUD/USD stood at 10.67% against 9.38% for the month.

Stimulus measures from China are having far reaching effects, including bolstering support for industrial metals. As a result, silver is on something of a tear right now, having tested two-month lows at the start of the week. That better-than-expected US PMI data did call time on the run higher, but Silver was noted as the most active commodity trade, with one day vol of 26.68% against 22.9% for the month.

Hopes of a rebound in China also served to buoy copper prices, with the underlying returning to levels not seen since the start of the year. One day vol on the trade came in at 17.34% against 15.82% for the month. Keeping with a theme, elevated levels of interest were sustained for Hong Kong stocks. Hopes are that cross-border listings will continue to find support off those stimulus moves, with the underlying Hang Seng index having traded in a range of almost 10% so far this week. One day vol stood at 42.89% against 27.67% for the month.